ChangXin Technology IPO Subscription Closes: First-Half Net Profit Expected to Exceed 50 Billion Yuan, Pre-Locks Tsinghua and Peking University Graduates to Solve Talent Shortage

ChangXin Technology (688825.SS), which carries the hopes of China’s domestic memory chip industry, is now turning its attention to talent reserves as a deeper competitive moat, even as its profitability hits record highs.

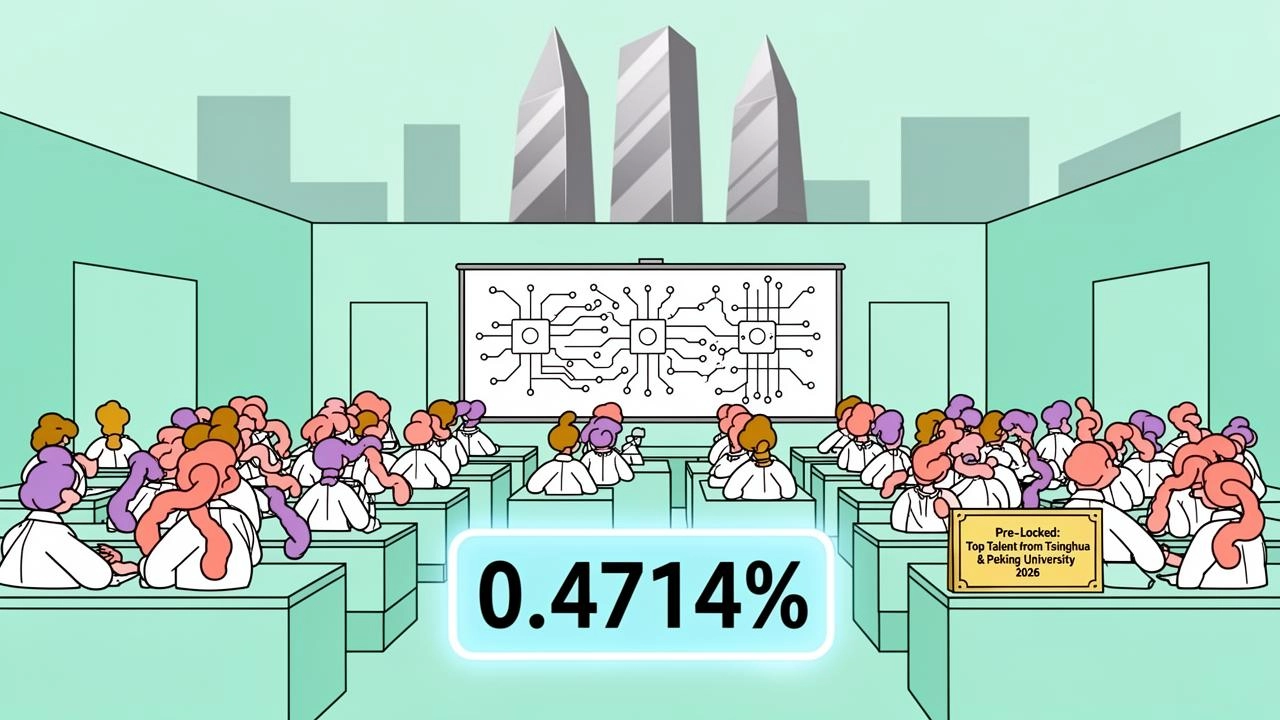

On the evening of July 16, ChangXin Technology disclosed the subscription details for its STAR Market online offering. The announcement showed an issue price of 8.66 yuan per share, with a staggering 9.43 million valid online subscription accounts and 816.92 billion shares validly subscribed. After triggering the clawback mechanism, the final online lottery rate stood at approximately 0.4714%. This marks the final sprint for ChangXin Technology’s entry into the capital markets — since its STAR Market IPO application was accepted in December 2025, the company has completed review, registration, and offering preparation in just about seven months.

Matching the frenzy of the IPO subscription is the overwhelming turnout at ChangXin Technology’s recent campus recruitment events across major universities. According to a report by Time Weekly, ChangXin’s information sessions were packed to capacity at several prestigious institutions. A source close to the company revealed that it has established a dedicated NCG (New College Graduate) training system and frequently runs pre-placement university-industry collaboration programs, with graduates predominantly coming from China’s top universities such as Tsinghua University and Peking University. The source noted bluntly that the semiconductor industry previously suffered from a talent gap, and ChangXin Technology now aims to build an industry “Whampoa Military Academy.”

Explosive Earnings Growth: Six-Month Profit Covers Three Years of Losses

ChangXin Technology is China’s largest DRAM (Dynamic Random Access Memory) manufacturer. According to Omdia, ChangXin Technology ranks fourth globally by production capacity and shipment volume. CFM Flash Market data shows that in the first quarter of 2026, ChangXin Technology’s DRAM sales revenue reached $7.309 billion, with its market share rising to 7.7%, behind only Samsung, SK Hynix, and Micron.

In this upcycle for the memory industry, ChangXin Technology’s performance has been nothing short of stunning. The company expects first-half 2026 revenue of 110 billion to 120 billion yuan (approximately $16.2 billion to $17.7 billion), representing more than sixfold year-on-year growth. Net profit attributable to parent company shareholders is projected between 50 billion and 57 billion yuan (approximately $7.4 billion to $8.4 billion). Based on these preliminary estimates, just the first half of this year’s profit would be sufficient to cover the cumulative losses of the past three years.

The prospectus data clearly outlines ChangXin Technology’s profit recovery trajectory: from 2023 to 2025, the company’s net profits were -19.23 billion yuan (approximately $2.8 billion), -9.05 billion yuan (approximately $1.3 billion), and 7.14 billion yuan (approximately $1.1 billion), respectively. For a memory chip company that has long relied on capital investment to chase overseas giants, this signals that its domestic DRAM business is entering a phase of commercial monetization.

Huang Lichong, President of Huisheng International Capital, analyzed that judging whether the profit turnaround is sustainable requires looking beyond memory prices to unit costs, the revenue share of advanced products, and operating cash flow. “The industry cycle is only an external factor for profit improvement; the company’s own capability enhancement determines whether profits can truly be realized.”

Data shows that in 2025, while ChangXin Technology’s DDR product unit prices rose 61%, unit costs fell 26.26%; LPDDR product unit prices rose 24.46%, while unit costs dropped 22.85%. The company’s consolidated gross margin surged from -1.93% in 2023 to 40.99% in 2025, approaching the levels of overseas giants like Samsung and Micron. In Huang Lichong’s view, this reflects the combined effect of economies of scale, yield improvement, lean manufacturing, and the rapid ramp-up of high-margin DDR5 products.

Talent Supply Lags Behind, Academia-Industry Disconnect a Key Pain Point

What is harder to obtain than chips are the people who make them.

Unlike the internet and software industries, DRAM manufacturing demands from engineers something closer to a “long-term craft.” From materials, physics, and chemistry to circuit design, manufacturing processes, and equipment debugging, nearly every link requires interdisciplinary knowledge and relies heavily on hands-on experience accumulated on high-cost production lines. A mature engineer often takes several years to develop.

Zhang Xiaorong, Director of the Deep Tech Research Institute, told Time Weekly that China’s current semiconductor talent cultivation still suffers from a significant disconnect between academia and industry. “What schools teach and what the industry needs are two different things. Textbooks are still covering 40nm processes while production lines have already reached 5nm. Graduates entering factories need 3-5 years of retraining.”

Semiconductor veteran expert Zhang Guobin further explained that DRAM is one of the most complex categories in semiconductor manufacturing, involving tens of thousands of process steps. However, China previously had no mass-production DRAM lines, so universities and research institutions could only teach theoretical knowledge, unable to provide real-world experience in process tuning, yield ramp-up, and failure analysis.

The talent development cycle is equally lengthy. Industry insiders generally believe that a DRAM engineer’s growth cycle almost mirrors the development cycle of a product generation: being able to independently handle a single process step typically takes 2-3 years; becoming a core engineer involved in yield optimization takes 5-8 years; and a technical leader capable of overseeing R&D, process iteration, and mass production systems often requires 8-12 years, having fully experienced multiple generations of product development and mass production.

From “Poaching” to “Cultivating,” ChangXin Seeks to Build a Talent Moat

Faced with the reality that talent supply is far outpaced by industry expansion demand, ChangXin has chosen to extend talent cultivation upstream rather than passively waiting for mature engineers to enter the market.

Lu Hong, founder of M&A Talent, analyzed to Time Weekly that the standardized full-cycle training system established by ChangXin — such as the “18-month NCG Program” and the “dual-track promotion mechanism” — combined with China’s only 12-inch DRAM mass production platform, gives it a supply-chain-leader-level talent incubation capability. Compared to production capacity, equipment, and capital, the ability to continuously cultivate DRAM engineers may be an even harder-to-replicate moat for China’s domestic memory industry.

Zhang Guobin revealed that ChangXin Memory Technologies (a subsidiary of ChangXin Technology) was the first company in mainland China to achieve DRAM mass production; prior to this, mainland China had virtually no talent pool with DRAM fab experience. ChangXin’s early core team recruited a large number of engineers from TSMC, UMC, Micron, Samsung, and SK Hynix, while also absorbing a group of local senior personnel with fab experience, forming China’s earliest DRAM mass production talent cluster.

The source close to ChangXin Technology believes that the company’s NCG training system is the first wave of training for graduates, and the difficulty of DRAM directly elevates talent capabilities to a very high level, laying a technical talent foundation for the entire industry. “The process difficulty of DRAM is compatible with other categories, so talent cultivation is not just for ChangXin itself, but for the entire industry.”

However, whether ChangXin can truly become the industry’s “Whampoa Military Academy” remains a subject of debate within the industry. Zhang Guobin pointed out that DRAM processes are highly customized, with each company maintaining strict technology confidentiality and patent barriers. ChangXin’s DRAM process started from external technology licensing and gradually evolved to its proprietary “MX” process platform, which is not fully compatible with the technology paths of Samsung and SK Hynix. These technological barriers somewhat limit the universality of talent spillover. In his view, ChangXin is more like a “DRAM talent boot camp” — it has indeed cultivated a batch of China’s most scarce DRAM mass production talent, but a systematic, exportable mature talent cultivation paradigm has yet to fully take shape.

Strong Cyclicality Shadow Lingers, Earnings Sustainability Awaits Test

Even with significantly improved profitability, ChangXin Technology still cannot fully escape the impact of the DRAM industry’s strong cyclicality.

ChangXin Technology Chairman Zhu Yiming candidly stated at a July 15 investor communication meeting that since the second half of 2025, the company’s performance growth has benefited from AI-driven DRAM demand explosion and tight industry supply-demand dynamics, but the DRAM industry is highly cyclical with significant price volatility, and AI development also brings uncertainty to market demand. If adverse macroeconomic changes occur, AI demand falls short of expectations, or new capacity is released in a concentrated manner, the industry could still return to a downcycle.

High fixed asset depreciation is a persistent pressure ChangXin Technology must face. The prospectus shows that from 2023 to 2025, the company’s fixed asset depreciation was 10.56 billion yuan (approximately $1.6 billion), 14.88 billion yuan (approximately $2.2 billion), and 24.68 billion yuan (approximately $3.6 billion), respectively. As of December 31, 2025, its cumulative uncovered losses still amounted to 36.65 billion yuan (approximately $5.4 billion), primarily because the DRAM industry is heavily scale-oriented, requiring continuous capacity expansion, while fab construction brings enormous fixed asset investment and depreciation pressure.

For this STAR Market IPO, ChangXin Technology plans to raise 29.5 billion yuan (approximately $4.4 billion). Of this, 7.5 billion yuan (approximately $1.1 billion) will be used for wafer manufacturing mass production line technology upgrades, 13 billion yuan (approximately $1.9 billion) for DRAM technology upgrades, and 9 billion yuan (approximately $1.3 billion) for forward-looking technology R&D. The listing is not just a fundraising event, but a critical milestone for ChangXin Technology to further close the gap with overseas giants.

From a global competitive landscape perspective, in the fourth quarter of 2025, ChangXin Technology’s global DRAM sales revenue market share was approximately 7.67%, while Samsung, SK Hynix, and Micron held 33.96%, 34.48%, and 23.41%, respectively. Guolian Minsheng Securities forecasts that as multi-site capacity deployment advances, ChangXin Technology’s global market share could reach 17% by 2028.

Huang Lichong noted that ChangXin Technology has crossed the “zero to one” stage for domestic DRAM, but there is still a gap before becoming a global top-tier player. The next phase requires closing the gap in large-scale stable mass production capability of advanced processes, with core metrics being yield and cost per bit, while also needing to enhance its high-end product mix, global customer resources, and advanced packaging capabilities.

As the AI industry rapidly develops, memory chips are becoming a new competitive battleground. Overseas memory giants have in recent years been positioning for the AI market through high-value-added products like HBM (High Bandwidth Memory) to mitigate the impact of traditional DRAM cyclical fluctuations. In comparison, ChangXin Technology’s AI-related revenue share remains relatively low, and it has yet to disclose any significant HBM revenue. Zhang Yi, CEO of iiMedia Research Group, stated that going forward, ChangXin Technology needs to rely on a “dual-track layout” of traditional DRAM iteration and AI high-end memory R&D: in the short term, stabilizing its foundation through DDR5 product mix upgrades, and in the medium to long term, driving the industrialization of HBM and other AI high-value-added memory products, which will be a key direction for the company to further narrow the gap with international leading players.